The above figure shows the market for gasoline. When a hurricane destroys a major refinery that refines oil into gasoline, the

A) demand curve for gasoline shifts from D1 to D2 and the supply curve of gasoline does not shift.

B) demand curve for gasoline shifts from D1 to D2 and the supply curve of gasoline shifts from S2 to S1.

C) demand curve for gasoline does not shift, and the supply curve of gasoline shifts from S2 to S1.

D) demand curve for gasoline does not shift, and the supply curve of gasoline shifts from S1 to S2.

C

You might also like to view...

The Grangers were the first farm organization of importance and are noted for

a. encouraging the federal government to re-issue "greenbacks.". b. establishing cooperatives that sold farm and consumer goods to their members. c. refusing to sell grain to foreign countries. d. forming a cartel that set upper limits on members' output of basic farm products. e. All of the above.

The Budget Enforcement Act of 1990: a. was a package of spending cuts and tax increases designed to reduce budget deficit

b. succeeded in balancing the budget cyclically. c. succeeded in balancing the budget within two years. d. identified defense and international programs as the only two areas of potential spending cuts. e. gave the President the authority to make unilateral spending cuts to balance the budget.

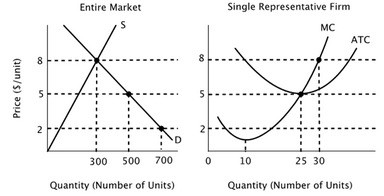

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves. Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

A. It is impossible to determine whether the number of firms in this market will rise or fall. B. The number of firms in the market will rise as firms enter the market in response to positive economic profit. C. The number of firms in the market will fall as firms exit the market in response to negative economic profit. D. The number of firms in the market will not change unless there is a change in either demand or in the cost of production.

Consumers gain from trade within a monopolistically competitive industry because:

a. prices fall and product varieties decrease. b. prices rise and product varieties increase. c. prices rise and product varieties decrease. d. prices fall and product varieties increase.