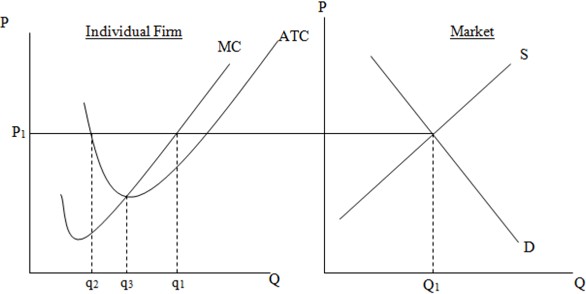

In the long run, the typical firm in this market will produce a quantity equal to

A. q3.

B. q2.

C. q1.

D. Q1.

Answer: A

You might also like to view...

Which of the following statements is true?

A) The marginal cost curve intersects the average fixed cost curve at its minimum point. B) When marginal cost is greater than average fixed cost, average fixed cost increases. C) Average fixed cost does not change as output increases. D) As output increases, average fixed cost becomes smaller and smaller.

A curve that shows how the best available consumption bundle changes as income changes (holding the consumer's preferences and all other prices fixed) is called:

A. a price-consumption curve. B. an individual demand curve. C. an income-consumption curve. D. a budget line.

Which question is an illustration of a microeconomic question?

a. Is the quantity of wine purchased in one year dependent upon the price of wine? b. Is the purchasing power of the dollar higher or lower today than it was in 2000? c. Does government spending influence the total level of employment in the economy? d. Is capitalism superior to socialism?

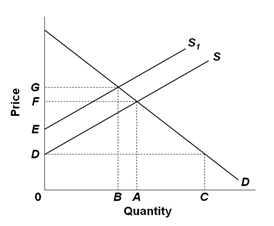

Refer to the supply and demand graph below. In the graph, line S is the current supply of this product, while line S1 is the optimal supply from the society's perspective. This figure suggests that there is (are):

A. External benefits from the production of this product

B. External costs in the production of this product

C. Currently an underallocation of resources toward producing this good

D. Positive externalities from producing the good