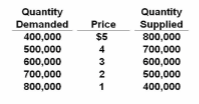

Refer to the table. If each of the 100 firms in the industry is maximizing its profit and earning only a normal profit, each must have an average total cost of:

A. $2.

B. $3.

C. $4.

D. $5.

B. $3.

You might also like to view...

The long run is a time frame in which

A) the quantities of some factors of production are fixed and the quantities of other factors of production can be varied. B) the quantities of all factors of production can be varied. C) the quantities of all factors of production are fixed. D) all costs are sunk costs.

At the competitive market outcome in the above figure, the

A) producer surplus is equal to $480 million. B) total producer surplus from turkey sales is zero. C) sum of consumer and producer surpluses from turkey is $640 million. D) All of the above answers are correct.

Fiscal policy cannot help an economy produce at an output level above potential GDP without causing __________.

a. inflation b. deflation c. unemployment d. taxation

Suppose there is a 30% chance that an oil spill will occur in an area and the economic damage of the potential spill is $1 million. What is the expected value associated with the spill?

a. $3,000,000 b. $1,000,000 c. $300,000 d. $30,000 e. $3,000