The loss minimization point for a firm is

A. when at the minimum point on the average total cost curve.

B. when at the minimum point on the average variable cost curve.

C. where marginal cost equals marginal revenue.

D. when total revenue is maximized.

C. where marginal cost equals marginal revenue.

You might also like to view...

For the U.S. economy, on an average:

A) growth resulting from technology is greater than the growth resulting from human capital. B) growth resulting from technology is smaller than the growth resulting from physical capital. C) growth resulting from technology equal to the growth resulting from physical capital. D) growth resulting from technology equal to the growth resulting from human capital.

With respect to production, the short run is best defined as a time period

A) lasting about six months. B) lasting about two years. C) in which all inputs are fixed. D) in which at least one input is fixed.

Social insurance programs are designed to provide financial assistance to people who have fallen into poverty

Indicate whether the statement is true or false

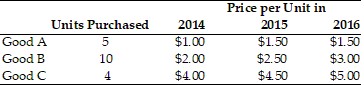

Refer to the information provided in Table 22.6 below to answer the question(s) that follow.

Table 22.6 Refer to Table 22.6. The bundle price for the goods in period 2014 is

Refer to Table 22.6. The bundle price for the goods in period 2014 is

A. $41.00. B. $50.50. C. $57.50. D. $100.00.