When economic profits are zero for a firm in a perfectly competitive market, it means that:

A. average total costs are zero.

B. price is equal to minimum average total cost.

C. MR is equal to AVC.

D. average variable costs are minimized.

Answer: B

You might also like to view...

When the price of a product is increased 15%, the quantity demanded decreases 10%. We can therefore conclude that the demand for this product is

A. cross-elastic. B. unitary elastic. C. inelastic. D. elastic.

What factors cause private and social rates of return for primary and secondary education to diverge in developing countries?

What will be an ideal response?

Suppose the market demand curve is given by Qd = 80 - 10P, and the market supply curve is given by Qs = 10 + 15P. What is the equilibrium price and quantity?

A. P* = $2.80 and Q* = 54 B. P* = $2.80 and Q* = 52 C. P* = $2.60 and Q* = 54 D. P* = $3.00 and Q* = 55

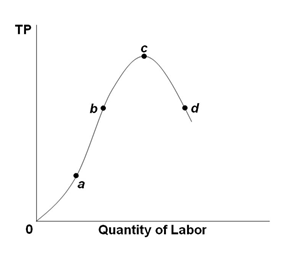

Refer to the graph below. It shows the total product (TP) curve. At which point is marginal product smallest?

A. Point a

B. Point b

C. Point c

D. Point d