The table below shows a pizzeria's fixed cost and variable cost at different levels of output. Pizza's sell for $20 each.Number ofPizzas Per DayFixed Cost($/Day)Variable Cost($/Day)050002550015050500250755004501005008501255001,650When the pizzeria makes 100 pizzas a day, its fixed cost is ________ and its total cost is ________.

A. $850; $1,650

B. $500; $850

C. $350; $850

D. $500; $1,350

Answer: D

You might also like to view...

What was the Industrial Revolution? How did it contribute to modern economic growth?

What will be an ideal response?

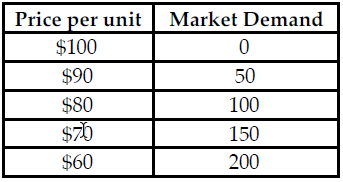

Refer to the table below. If this market is a Cournot Oligopoly and Firm X is produces 50 units, what is Firm Y's profit-maximizing quantity if their average total and marginal cost are constant and equal to $40?

The table above shows the market demand for a product that both Firm X and Firm Y manufacture. Both firms produce an identical product and the firms' average total and marginal cost are equal and constant.

A) 150 B) 50 C) 200 D) 100

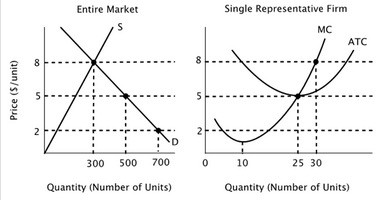

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves. In the long run equilibrium in this market:

In the long run equilibrium in this market:

A. price will equal $5, and there will be 20 firms in the industry. B. price will equal $5, and there will be 10 firms in the industry. C. price will equal $5 and total output will equal 500 units, but there is not enough information to determine how many firms will be in the industry. D. price will equal $8, and there will be 20 firms in the industry.

Which of the following is an endogenous variable in our model of the goods market in Chapter 3?

A) consumption (C) B) disposable income (YD) C) saving (S) D) total income (Y) E) all of the above