To economists, the main difference between the short run and the long run is that:

A. the law of diminishing returns applies in the long run, but not in the short run.

B. in the long run all resources are variable, while in the short run at least one resource is

fixed.

C. fixed costs are more important to decision making in the long run than they are in the short

run.

D. in the short run all resources are fixed, while in the long run all resources are variable.

Answer: B

You might also like to view...

Suppose that the market for salad dressing is in equilibrium. Then the price of lettuce rises. What will happen?

A. The quantity demanded of salad dressing will increase. B. The supply of salad dressing will decrease. C. The demand for salad dressing will decrease. D. The price of salad dressing will rise.

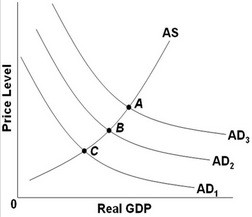

Refer to the above diagram. The economy is at equilibrium at point B. What fiscal policy would increase real GDP?

Refer to the above diagram. The economy is at equilibrium at point B. What fiscal policy would increase real GDP?

A. Decrease aggregate demand from AD2 to AD3 by decreasing government spending. B. Increase aggregate demand from AD2 to AD3 by decreasing taxes. C. Increase aggregate demand from AD2 to AD1 by decreasing taxes. D. Decrease aggregate demand from AD2 to AD3 by increasing government spending.

According to the Ricardian equivalence proposition, a temporary government budget deficit created by cutting taxes

A. will cause future taxes to increase but will have no real economic effects. B. will have the same real economic effects as a budget deficit created by raising government spending. C. would have the same real effects whether or not consumers expect future taxes to change. D. will cause desired consumption to increase.

The principal economic cost of growth is:

A. higher interest rates B. higher inflation rates C. higher unemployment rates D. consumption sacrificed for capital formation