In perfect competition, all the following situations arise except ________

A. firms produce an identical good or service

B. each firm chooses the price at which to sell the good it produces

C. firms can sell any quantity they choose to produce at the market price

D. buyers know each seller's price

B Firms in perfect competition are price takers so they "take" the price determined in the market.

You might also like to view...

Depository institutions do all of the following EXCEPT

A) set the required reserve ratio. B) create liquidity. C) pool risks. D) minimize the cost of obtaining funds.

A monopolistically competitive firm is similar to

A) a monopoly in the short run because it can make an economic profit in the short run and is similar to a perfectly competitive firm in the long run because it cannot make a positive economic profit. B) a perfectly competitive firm in the short run because it cannot make an economic profit in the short run and is similar to a monopoly in the long run because it can make an economic profit. C) a monopoly because it can make an economic profit in both the short run and long run. D) a perfectly competitive firm because its economic profit is equal to zero in both the short run and long run.

The "underground economy" is also referred to as

A) the informal sector. B) the halfway economy. C) the net domestic product economy. D) the formal sector.

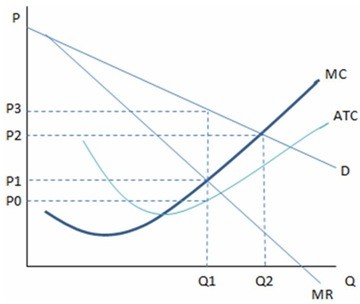

This graph shows the cost and revenue curves faced by a monopoly.  According to the graph shown, if Q2 units are being produced, this monopolist:

According to the graph shown, if Q2 units are being produced, this monopolist:

A. should cut back production to increase profits. B. is maximizing profits. C. is maximizing revenue. D. is earning negative profits.