If, as a perfectly competitive industry expands, it can supply larger quantities only at a higher long-run equilibrium price, it is

A) a constant-cost industry.

B) an increasing-cost industry.

C) a decreasing-cost industry.

D) a fixed-cost industry.

Answer: B

You might also like to view...

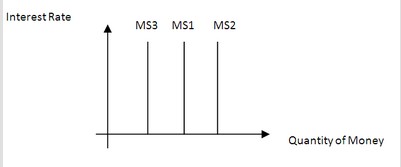

Use the following diagram to answer the next question. Which of the following would cause a move from MS1 to MS3?

Which of the following would cause a move from MS1 to MS3?

A. The banking system decides to hold less excess reserves and make more loans. B. The reserve requirement is reduced by the Board of Governors. C. The Federal Open Market Committee decides to sell bonds. D. The discount rate is decreased by the regional Federal Reserve banks.

A tax that imposes a small excess burden relative to the tax revenue that it raises is

A) an efficient tax. B) a payroll tax. C) a sin tax. D) a FICA tax.

Conditional probability of event A given that event B has already occurred is represented as the ratio between Pr[A and B] and Pr[B]

Indicate whether the statement is true or false

Horizontal equity is a difficult concept to implement because

A. it is difficult to determine how unequally unequals should be treated. B. it is difficult to measure ability to pay. C. it is difficult to determine which people are equally situated. D. people object to the use of absolute tax liability instead of percentage of income.