The Law of Supply states that, other things being constant, when the price of a good increases then;

a) Supply and demand both decrease.

b) Demand increases and supply decreases.

c) The quantity demanded decreases.

d) The quantity supplied increases.

Answer: d) The quantity supplied increases

You might also like to view...

Gross Domestic Product includes the sale of intermediate goods and services

a. True b. False Indicate whether the statement is true or false

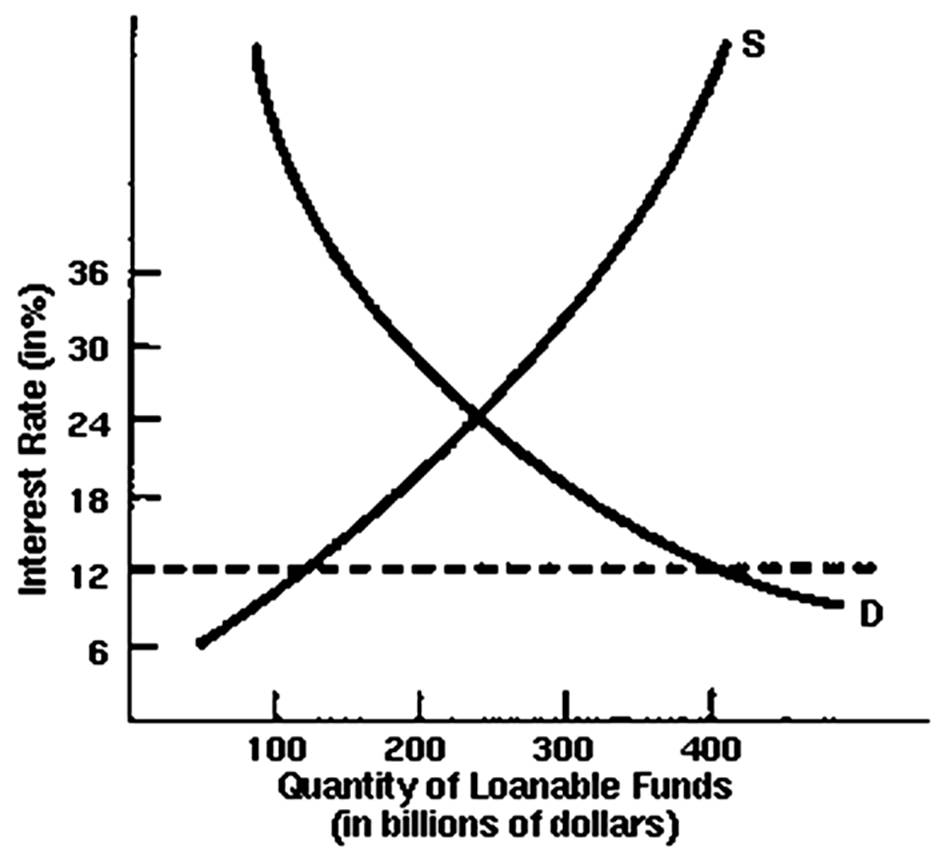

How much would the interest rate be if there was no usury law?

Suppose the w = $20 and r = $30. The isocost line for a firm in this industry is:

A. K = 0.033C ? 0.66L. B. 1.5L + K = 0.5C. C. C = 20K + 30L. D. Depends entirely on the functional form of the production function.

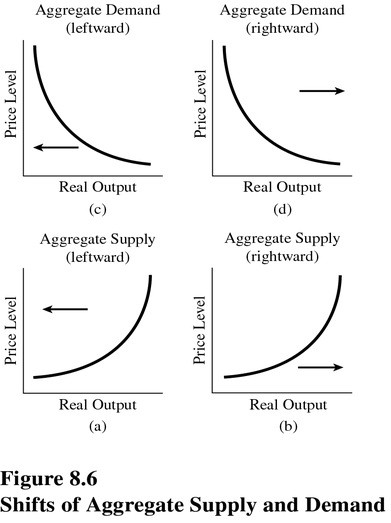

Choose the letter below that best represents the type of shift that would occur in the following situation in the United States: During the late 1990s, productivity in many U.S. industries increased because of technological advances. (See Figure 8.6.)

Choose the letter below that best represents the type of shift that would occur in the following situation in the United States: During the late 1990s, productivity in many U.S. industries increased because of technological advances. (See Figure 8.6.)

A. A. B. B. C. C. D. D.