A price ceiling is

A. a maximum price set by government that sellers may charge for a good.

B. the minimum price that consumers are willing to pay for a good.

C. the difference between the initial equilibrium price and the equilibrium price after a decrease in supply.

D. a minimum price set by government that sellers may charge for a good.

Answer: A

You might also like to view...

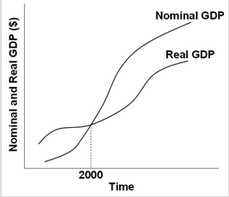

Use the following graph to answer the next question.  Which of the following statements is correct on the basis of the information shown?

Which of the following statements is correct on the basis of the information shown?

A. The GDP price index equals 100 in 2000. B. The GDP price index is less than 100 in 2010 C. The GDP price index is greater than 100 in 1990. D. Without additional data, the value of the GDP price index cannot be known for any year in the graph above.

Describe and explain the relationship between the price of bonds and the interest rate

What will be an ideal response?

Suppose the price of lumber decreases. In the market for new homes, we would expect which of the following to occur?

A) the market clearing price will fall and the equilibrium quantity will rise. B) the market clearing price will rise and the equilibrium quantity will fall. C) both the market clearing price and the equilibrium quantity will fall. D) both the market clearing price and the equilibrium quantity will rise.

When a decrease of a firm's scale of production leads to lower average costs per unit produced, there is an increasing return to scale.

Answer the following statement true (T) or false (F)