A natural oligopoly occurs when

a. few firms can afford to compete in the industry

b. the minimum efficient scale is a large fraction of the market

c. there are a large number of buyers and sellers of a standardized product

d. minimum efficient scale is greater than total market demand at the price equal to minimum long run average total cost

e. competitive pricing drives firms from the market

B

You might also like to view...

It is often observed that, over the same period of time and for the same good, marginal utility declines rapidly for some consumers and very little for others. This observation illustrates:

a. that economic theory is of little value in explaining consumer behavior. b. that consumers are not identical. c. tastes and preferences should not be included in any discussion of consumer choice. d. tastes and preferences among consumers are quite similar. e. that if consumers weren't identical, economic theory would not be able to provide insight into consumer behavior.

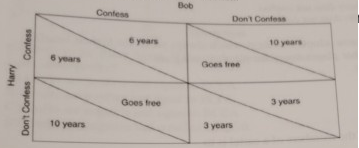

The figure gives the payoff matrix for two individuals who are being accused of robbing a bank together. What is dominant strategy for Bob?

A) Confess.

B) Don't confess.

C) Flip a coin to decide what to do.

D) There is no dominant strategy.

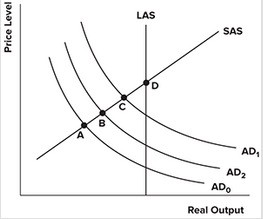

Refer to the graph shown. Assume the economy is in short-run equilibrium at point A below potential output. The government opts for an expansionary fiscal policy in an attempt to pull the economy out of the recession. An economist with a Classical view holding the Ricardian equivalence theorem to be practically true would conclude that the economy will most likely end up at point:

A. A. B. B. C. C. D. D.

Based on Scenario 6.1 above, value added in the United States is

A) $500. B) $600. C) $400. D) $300.