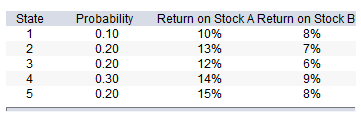

Let G be the global minimum variance portfolio. The weights of A and B in G are __________ and __________, respectively.

Consider the following probability distribution for stocks A and B:

A. 0.40; 0.60

B. 0.66; 0.34

C. 0.34; 0.66

D. 0.77; 0.23

E. 0.23; 0.77

E. 0.23; 0.77

wA = [(1.1)2 – (1.5)(1.1)(0.46)]/[(1.5)2 + (1.1)2 – (2)(1.5)(1.1)(0.46) = 0.23; wB = 1 – 0.23 = 0.77.

You might also like to view...

Earned media is a favorite choice among public relations practitioners because it is guaranteed

Indicate whether the statement is true or false

Troy, a technical writer, is most likely to experience carpal tunnel syndrome when he is angry about being given so few interesting assignments

Indicate whether the statement is true or false.

A segment of a business responsible for both revenues and expenses would be called:

A. a cost center. B. residual income. C. an investment center. D. a profit center.

A survey of an entire population is called

a. population analysis b. population c. census d. target population