In a short-run production process, the marginal cost is rising and the average variable cost is falling as output is increased. Thus,

A) average fixed cost is constant.

B) marginal cost is above average variable cost.

C) marginal cost is below average fixed cost.

D) marginal cost is below average variable cost.

D

You might also like to view...

The production of paper creates pollution, an external cost. What happens to the production of paper if the government imposes a tax on paper producers equal to the marginal external cost of the pollution?

What will be an ideal response?

Answer the following statements true (T) or false (F)

1. Raising taxes in order to pay off the U.S. national debt would result in a significant redistribution of income. 2. Passing the debt on to future generations has a different impact on individuals than it does on the total economy. 3. Reducing the national debt would increase the money supply. 4. The actual deficit is a poor measure of fiscal policy. 5. The U.S. national debt has declined continuously as a percentage of GDP since World War II.

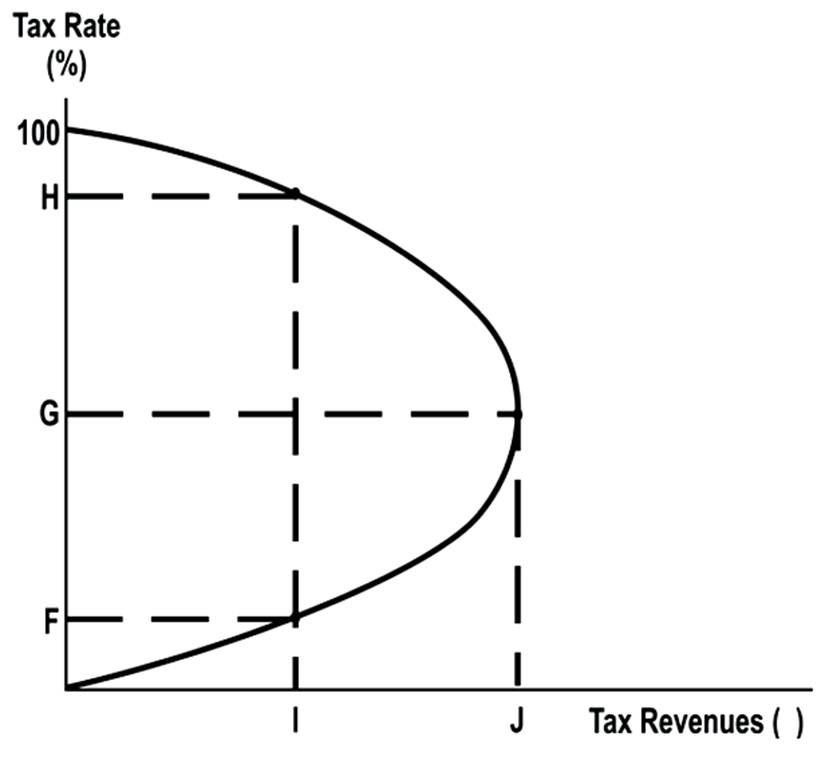

Which tax revenue given in the graph will be generated by two different tax rates?

A. F

B. G

C. H

D. I

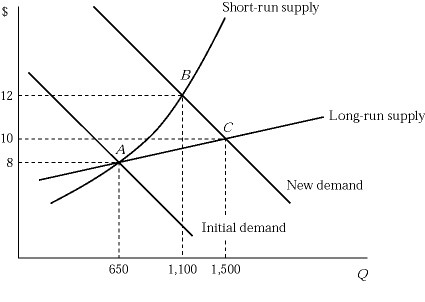

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the short run?

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the short run?

A. The market price rises to $12, which is greater than the average total cost. B. Each existing firm maximizes its profit by producing the output where marginal cost equals $12. C. Each existing firm produces two more units per hour, compared to its initial profit-maximizing output level at point A. D. All of these are correct.