The resources used to make all goods and services are the:

a) production possibilities

b) factors of production

c) production trade-offs

d) opportunity costs

Ans: b) factors of production

You might also like to view...

Excess reserves immediately decrease if

A) reserve requirements increase. B) reserve requirements decrease. C) the discount rate increases. D) the discount rate decreases.

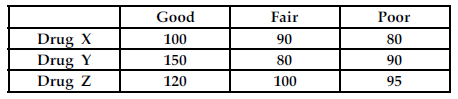

Refer to the table below. If the senior manager learns that either a Fair or Poor market will exist when the drug is introduced to the market, which drug should the senior manager pursue?

The senior manager of Rx Pharmaceuticals needs to decide which of three drugs the company should consider developing. The estimated profit for each of the drugs differs depending on the market conditions when the respective drugs are introduced to the market. The above table summarizes the estimated profit for each drug under each of the three market conditions; Good, Fair, and Poor.

A) Drug Z

B) Drug X

C) Drug Y

D) none of the drugs

In a typical economy, the dollar value of the total output for a period will equal the sum of consumption spending, planned investment spending, government spending, and net tax revenue

a. True b. False

A firm has positive fixed cost and positive variable cost. At its current level of output, marginal cost equals average cost. The firm must

a. not be producing at its profit-maximizing level of output. b. be producing the quantity that minimizes average cost. c. be operating at a point at which total variable cost equals total fixed cost. d. be earning negative profit.