Which of the following is true in the long run?

A) Total cost equals fixed cost.

B) Total cost is constant.

C) All costs are variable.

D) Marginal cost equals zero.

E) None of the above is true in the long run.

C

You might also like to view...

Refer to the figure above. What is the domestic demand for calculators in Barylia, once the economy opens up to free trade?

A) 20 units B) 50 units C) 60 units D) 100 units

Fashion trends are a nonprice determinant for demand because

A) they cause a movement along the demand curve. B) they influence people's tastes and preferences in clothing. C) they change the supply of accessories. D) they do not affect demand.

Cooperative efforts to establish a regional free trade area in the Asian-Pacific corridor have been hampered by perceived security threats posed by China and Japan as well as

a. fears of fragmenting the global trading system. b. existing relationships with the U.S. as a trading partner. c. the current Trans Pacific Partnership. d. the wide range of forms of government.

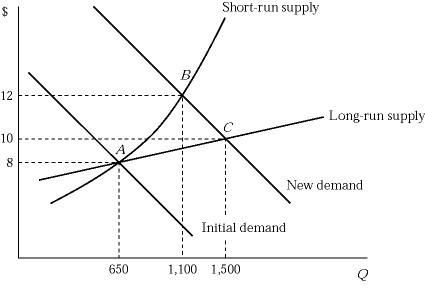

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the long run?

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the long run?

A. The market price drops below $12 as more firms enter the market and build more plants. B. Both existing firms and new firms earn a zero economic profit. C. All firms in the industry maximize their profits by producing the output where the marginal cost equals $10. D. All of these are correct.