If firms in a perfectly competitive industry are earning positive economic profits, then what will happen in the long run?

What will be an ideal response?

Economic profits provide incentives for entrepreneurs to start new firms and enter the industry. When entry of new firms takes place, the market supply curve shifts outward. The equilibrium quantity increases, and the market clearing price declines. This pushes economic profits back down toward zero. When economic profits return to zero, there is no longer an incentive for new firms to enter the industry, and a new long-run equilibrium will have been reached.

You might also like to view...

What action should the Fed take if it wants to move from a point on the short-run Phillips curve representing low unemployment and high inflation to a point representing higher unemployment and lower inflation?

What will be an ideal response?

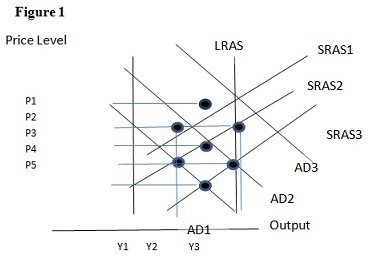

Using Figure 1 above, if the aggregate demand curve shifts from AD2 to AD3 the result in the short run would be:

A. P1 and Y2. B. P2 and Y3. C. P3 and Y1. D. P2 and Y2.

In perfect competition, environmental externalities need not distort the allocation of resources providing:

a. transactions costs are zero. b. average costs are constant for all output levels. c. firms install pollution control equipment. d. the government sets realistic pollution standards.

Public funding of stadium construction for a professional football, baseball or basketball team could be argued using "merit good" logic

Indicate whether the statement is true or false