Economists use the term imperfect competition to describe:

A. all industries that produce standardized products.

B. any industry in which there is no nonprice competition.

C. a pure monopoly only.

D. those markets that are not purely competitive.

Answer: D

You might also like to view...

Money is more mobile geographically now than in the past

Indicate whether the statement is true or false

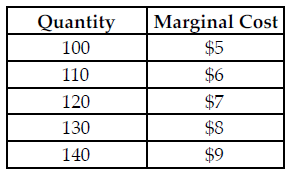

Refer to the table below. The perfectly competitive firm has a random demand with a 50 percent chance of being $5 and a 50 percent chance of being $7. What quantity should the firm produce to maximize its expected profit?

The above table summarizes the marginal cost of production at various quantity levels for a perfectly competitive firm.

A) 110

B) 120

C) 100

D) 130

If a purchase contract allows a buyer to accept less than a specified maximum "take" each month, buying a _____ would allow the seller to resell the excess at a _____ price

a. put option; profitable b. put option; predictable c. call option; predictable d. call option; profitable

Market signals

A. are best ignored by investors. B. are market noise that confuses buyers and sellers. C. always lead to economic losses. D. are ways of conveying information.