Answer the question on the basis of the following information. A farmer who has fixed amounts of land and capital finds that total product is 24 for the first worker hired; 32 when two workers are hired; 37 when three are hired; and 40 when four are

hired. The farmer's product sells for $3 per unit and the wage rate is $13 per worker. Refer to the given information. The marginal revenue product of the second worker is:

A. $24.

B. $8.

C. $15.

D. $9.

Answer: A

You might also like to view...

In the short run, a firm has fixed costs but never any variable costs

a. True b. False Indicate whether the statement is true or false

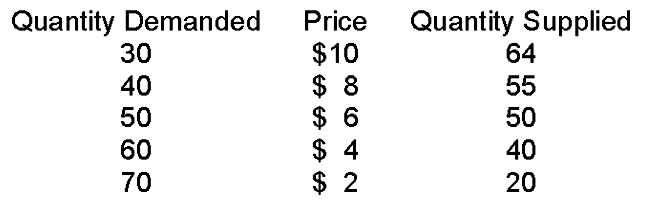

When the price is $2

A. quantity supplied is greater than quantity demanded and, therefore, price must rise to get to equilibrium.

B. quantity supplied is less than quantity demanded and, therefore, price must fall to get to equilibrium.

C. quantity demanded is greater than quantity supplied and, therefore, price must rise to get to equilibrium.

D. quantity demanded is greater than quantity supplied and, therefore, price must fall to get to equilibrium.

Standard & Poor's sells information to investors; this is their primary business. Is this an example of a financial intermediary? Explain.

What will be an ideal response?

Full-cost transfer-pricing creates an incentive for:

A. distribution to be over-efficient. B. distribution to be inefficient. C. manufacturing to be less efficient. D. manufacturing to be over-efficient.