When the market price rises, the consumers' consumer surplus ________. When the market price falls, the consumers' consumer surplus ________

A) decreases; increases

B) decreases; decreases

C) increases; increases

D) increases; decreases

E) does not change; increases

A

You might also like to view...

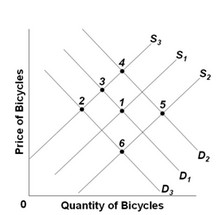

Use the following graph of the bicycle market to answer the question below. S1 and D1 are the original supply and demand curves. D2 and D3 and S2 and S3 are possible new demand and supply curves. Starting from the initial equilibrium (point 1), which point on the graph is most likely to be the new equilibrium after an increase in wages of bicycle workers and a significant increase in the price of gasoline?

S1 and D1 are the original supply and demand curves. D2 and D3 and S2 and S3 are possible new demand and supply curves. Starting from the initial equilibrium (point 1), which point on the graph is most likely to be the new equilibrium after an increase in wages of bicycle workers and a significant increase in the price of gasoline?

A. 4 B. 3 C. 5 D. 6

The above figure shows the market for a prescription drug. What is the equilibrium price of the drug? How many doses are purchased? Suppose the government imposes a price ceiling of $1.50 a dose

How many doses are purchased after the price ceiling is imposed?

Explicit costs are costs that:

A. require a firm to spend money. B. are zero when no output is produced. C. do not depend on the quantity of output produced. D. depend on the quantity of output produced.

The decision of which assumptions to make is

a. an easy decision for an economist, but a difficult decision for a physicist or a chemist. b. not a particularly important decision for an economist. c. usually regarded as an art in scientific thinking. d. usually regarded as the easiest part of the scientific method.