Brandon, Haley, Melissa, and Jeffrey each won $1,000 in their office football pool. According to Keynes's absolute income hypothesis, which of them would be most likely to spend the most out of their winnings?

a. Brandon, Haley, Melissa, and Jeffrey will spend the same out of their winnings

b. Brandon, who earns $10,000 as a mail clerk

c. Haley, who earns $25,000 as an account representative

d. Melissa, who earns $50,000 as a software programmer

e. Jeffrey, who earns $2 million as the CEO

B

You might also like to view...

An increase in the number of producers of a good will

a. increase the market supply because the price will rise b. increase the market supply only if market demand increases too c. increase the market supply because market supply is the sum of all individual supply curves d. increase the market supply only if all suppliers have an identical supply curves e. decrease the market supply because firms compete with each other and each firm will supply more

Applying the concept of opportunity cost to the pollution of a lake, an economist probably would conclude that:

A. pollution should be eliminated as long as the opportunity cost of a cleanup exceeds the cost of the resources required for the cleanup. B. pollution should be eliminated as long as the benefit from a cleanup exceeds the opportunity cost. C. no pollution in the lake should be eliminated regardless of benefit. D. all pollution in the lake should be eliminated regardless of cost.

If demand for a good is perfectly inelastic, then

A. a price increase would cause a fall in total revenue. B. a price increase would cause no change in quantity demanded. C. a price increase would cause an increase in quantity demanded. D. a price increase would cause a fall in quantity demanded.

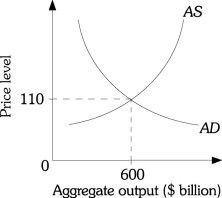

Refer to the information provided in Figure 26.6 below to answer the question(s) that follow. Figure 26.6Refer to Figure 26.6. Suppose the equilibrium price level is 110. An increase in the supply of oil would probably

Figure 26.6Refer to Figure 26.6. Suppose the equilibrium price level is 110. An increase in the supply of oil would probably

A. decrease both the equilibrium output and the price level. B. increase the equilibrium output and decrease the price level. C. decrease the equilibrium output and increase the price level. D. increase both the equilibrium output and the price level.