The law of diminishing marginal returns states

A) that at some point, adding more of a fixed input to a given amount of variable inputs will cause the marginal product of the variable input to decline.

B) that at some point, adding more of a variable input to a given amount of a fixed input will cause the marginal product of the variable input to decline.

C) that in the presence of a fixed factor, at some point average product of labor starts to fall as more and more variable inputs are added.

D) average total costs of production initially fall and after some point starts to rise at a decreasing rate as output increases.

Answer: B

You might also like to view...

How does the science of economics deal with the fact that we all have different values?

A) by assuming that values don't play a role in economic behavior B) by seeking to discover the sources of different value systems C) by using positive analysis D) by surveying the public to see what the most common values are, and then incorporating those as assumptions into their models

Suppose Frank quits his $25,000 a year job and starts his own hauling company. He takes $10,000 out of his savings account at the bank, where he was earning 5 percent interest, to buy a truck. His other expenses, including the truck, are $20,000 . Frank's revenues are $48,000 . Frank ends up with

a. $3,000 in wage-related rent b. $2,500 in entrepreneurial profit c. a $7,000 loss d. $48,000 in entrepreneurial profit e. $3,000 in entrepreneurial profit

Economic rent is the minimum payment necessary to induce any of the factor to be supplied.

Answer the following statement true (T) or false (F)

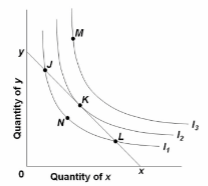

Refer to the diagram where xy is the relevant budget line and I 1 , I 2 , and I 3 are indifference curves. If the consumer is initially at point L, he or she should:

A. strive for point N by obtaining a larger money income.

B. purchase more of X and less of Y.

C. remain at that point to maximize utility.

D. purchase more of Y and less of X.