Suppose an increase in market demand occurs in a constant-cost industry. As a result

A. perfectly competitive firms will eventually enter the industry.

B. the new long-run equilibrium price will be lower than the original long-run equilibrium price.

C. equilibrium quantity will decline.

D. perfectly competitive firms will eventually leave the industry.

Answer: A

You might also like to view...

Exclusion by the BLS of which of the following tends to understate the measure of unemployment in the economy?

a. children b. retired persons c. students d. people who do not want to work e. discouraged workers

Which of the following statements about the public debt is? true?

A) It is equal to the budget deficit.

B) It decreases when the government runs a budget deficit.

C) It is a stock variable.

D) all of the above

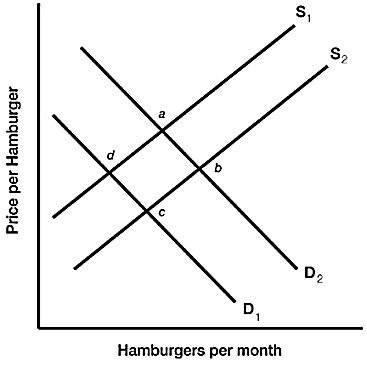

Figure 3.6 illustrates a set of supply and demand curves for hamburgers. An increase in supply and an increase in demand are represented by a movement from:

Figure 3.6 illustrates a set of supply and demand curves for hamburgers. An increase in supply and an increase in demand are represented by a movement from:

A. point d to point b. B. point d to point a. C. point c to point a. D. point b to point c.

A permanent reduction in international trade barriers would

A. decrease aggregate demand. B. increase aggregate demand. C. increase long-run aggregate supply. D. decrease long-run aggregate supply.