Which of the following statements about a monopolistically competitive firm, in the short run, is true?

a. Profits will be maximized at the point at which price equals marginal cost and hence there is no deadweight loss.

b. The firms earn zero economic profit in the short run.

c. The firms achieve allocative and productive efficiency in the short run.

d. Advertising may enable a firm to charge a higher price than that charged by rival firms.

e. It faces a perfectly elastic demand curve.

d

You might also like to view...

Which of the following will not reduce the likelihood of a principal-agent problem when getting your car repaired?

a. asking to see the replaced parts b. staying to watch the repair being done c. gathering information on car repair d. not paying until after the repair job is finished e. persuading the mechanic you know a lot about cars

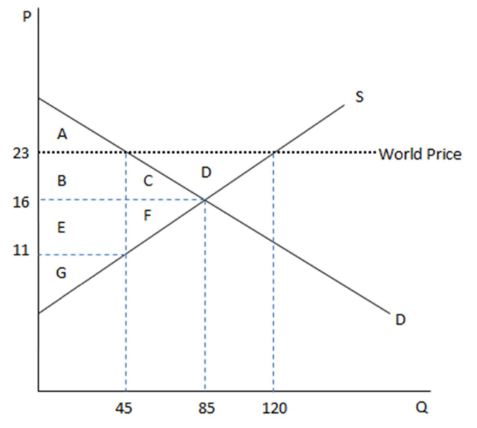

According to the graph shown, if this economy were an autarky, consumers would get area:

This graph demonstrates the domestic demand and supply for a good, as well as the world price for that good.

A. A in consumer surplus.

B. ABC in consumer surplus.

C. ABCD in consumer surplus.

D. ABCDEFG in consumer surplus.

If Alicia limits the range of her productive activities rather than trying to be self-sufficient, she is engaging in

a. specialization b. exchange c. absolute advantage d. increasing opportunity costs e. reducing her standard of living

Which of the following correctly describes the time-inconsistency problem?

a. The problem that arises when policy makers have an incentive to announce one policy to influence expectations, but then pursue different policy once those expectations have been formed and acted on. b. The problem that arises when the president and Congress have an incentive to pursue policies that are different from those of the Fed. c. The problem that arises when consumer preferences change frequently over time such that a product considered highly desirable at one point would be considered undesirable after sometime. d. The problem that arises when firms increase supply of a product in anticipation of future increase in demand for the product, but suffers a heavy loss because of a steep fall in demand.