If a product is narrowly defined, it is likely to

A) have many substitutes and therefore its demand is elastic.

B) have few substitutes, and therefore its demand is less elastic.

C) be unique, and therefore its demand is inelastic.

D) be unique and have many substitutes.

E) have a larger proportion of income spent on it.

A

You might also like to view...

If the two goods in an Edgeworth Box are perfect complements for both people, all efficient allocations will have each person getting the same amount of good 1 as of good 2.

Answer the following statement true (T) or false (F)

The Keynesian economic framework is based on the assumption that: a. prices and wages are sticky and do not adjust quickly

b. prices and wages self-adjust in the long run. c. agriculture is the source of economic wealth. d. markets work better without any government intervention.

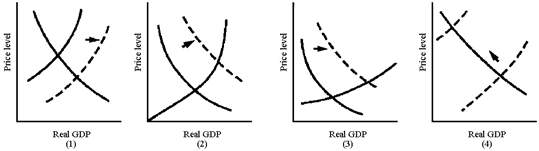

Figure 10-5

In Figure 10-5, which graph best illustrates the situation of an economy near full employment that experiences an increase in autonomous consumer spending?

a.

(1)

b.

(2)

c.

(3)

d.

(4)

Exhibit 2-11 Production possibilities curves In Exhibit 2-11, which of the following could have caused the production possibilities curve of an economy to shift from the one labeled A to the one labeled B?

In Exhibit 2-11, which of the following could have caused the production possibilities curve of an economy to shift from the one labeled A to the one labeled B?

A. A major natural disaster B. An increase in consumption goods production this year C. An advance in technology D. An increase in unemployment