Refer to the above figure. Suppose that the supply curve shifts from SA to SB while the demand curve shifts from DA to DB. Which of the following is TRUE about the results of the shifts in the supply and demand curves?

A) The equilibrium price increases while the equilibrium quantity remains unchanged.

B) Both the equilibrium price and equilibrium quantity increase.

C) The equilibrium price remains unchanged while the equilibrium quantity increases.

D) Both the equilibrium price and equilibrium quantity remain unchanged.

C

You might also like to view...

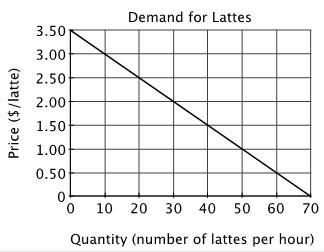

Refer to the figure below. If the price of a latte increases from $2.00 to $2.50:

A. the change in total expenditure, if any, would depend on the supply curve. B. total expenditure would stay the same. C. total expenditure would increase. D. total expenditure would decrease.

According to the textbook application, California’s urban smog problem

a. diminished because of the responsiveness of U.S. automobile manufacturers b. was never addressed by state legislation c. was linked through scientific study to auto emissions in the 1950s d. all of the above

The amount by which people will increase or decrease their purchases when prices change

A) is typically greater in the case of luxuries than in the case of necessities. B) is typically less for business firms than for households because business firms can more easily borrow to maintain purchasing patterns. C) is typically less for business firms than for households because business firms must have certain goods to remain in operation. D) tends to be greater over longer periods of time because it takes time to invent and to discover substitutes. E) will be approximately zero unless the demand also changes.

All firms in a competitive industry have the following long-run total cost curve:

C(q) = q3 – 10q2 + 36q where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like if this is a constant cost industry? Explain. b. Suppose the market demand is given by Q = 111 – p. Determine the long-run equilibrium number of firms in the industry.