Assume that Stanton's Equipment, Land and Trademark on the date of acquisition form part of a single asset group. Assume also that these assets are expected to generate future cash flows of $40,000. Does this mean that Stanton will have to recognize an impairment loss? Explain.

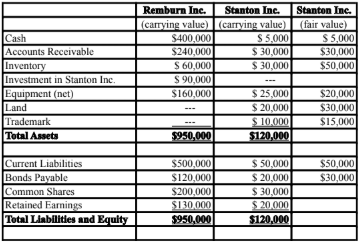

Remburn Inc. Inc. purchased 90% of the outstanding voting shares of Stanton Inc. for $90,000 on January 1, 2015. On that date, Stanton Inc. had common shares and retained earnings worth $30,000 and $20,000, respectively. The equipment had a remaining useful life of 10 years from the date of acquisition. Stanton's trademark is estimated to have a remaining life of 5 years from the date of acquisition. Stanton's bonds mature on January 1, 2035. The inventory was sold in the year following the acquisition. Both companies use straight line amortization, and no salvage value is assumed for assets. Remburn Inc. and Stanton Inc. declared and paid $12,000 and $4,000 in dividends, respectively during the year.

The balance sheets of both companies, as well as Stanton's fair values on the date of acquisition are shown below:

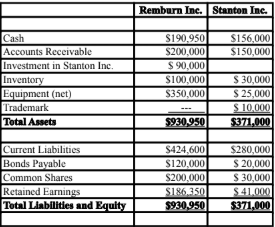

The following are the financial statements for both companies for the fiscal year ended December 31, 2015:

Income Statements

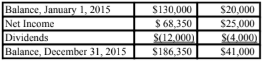

Retained Earnings Statements

Balance Sheets

Both companies use a FIFO system, and Stanton's entire inventory on the date of acquisition was sold during the following year. During 2015, Stanton Inc. borrowed $20,000 in cash from Remburn Inc. interest free to finance its operations. Remburn uses the Cost Method to account for its investment in Stanton Inc. Moreover,

Stanton sold all of its land during the year for $18,000. Goodwill impairment for 2015 was determined to be $7,000. Remburn has chosen to value the non-controlling interest in Stanton on the acquisition date at the fair value of the subsidiary's identifiable net assets (parent company extension method).

Not necessarily. Given the above information, Stanton has "failed" the first part of the required two-part impairment test required for long-lived assets since the expected future cash flows of this asset group of $40,000 falls well short of the carrying values of the assets within the group, which total $55,000. Given this information, the second part of the two-part impairment test must be applied.

The second part of the impairment test requires that an impairment loss be recognized if Stanton fails the first part of the impairment test and the fair values of the assets within the group are less than their total carrying values. However, since the fair values of the assets are higher than their carrying values ($65,000

vs. $55,000 respectively), there would be no impairment loss in this case.

You might also like to view...

The F distribution is a skewed distribution useful for testing equality of variances.

Answer the following statement true (T) or false (F)

People with low self-esteem ______ than those with higher self-esteem.

A. are more dependent on others B. choose more unconventional jobs C. focus more on their strengths D. handle failure better E. exhibit more aggressive behavior

Cost per rating point (CPRP) is calculated as:

A) cost of media buy divided by the vehicle's rating B) cost of media buy multiplied by the number of viewers C) ratings divided by gross exposures D) cost of media buy divided by gross exposures

Which of the following is not an essential feature of a disaster recovery plan?

a. off-site storage of backups b. computer services function c. second site backup d. critical applications identified