Two firms compete in a market by selling imperfect substitutes. The demand equations are given by the following equations:

Q1 = 50 - p1 + p2

Q2 = 50 - p2 + p1

For now, assume that each firm has a marginal cost and average cost of 0.

a. From the equations, how can you tell these goods are substitutes? How can you tell they are imperfect substitutes?

b. Suppose the firms compete by simultaneously choosing price. Find the best response function of each firm as a function of the other firm's price.

c. Compute the equilibrium price and quantity for each firm.

d. Suppose firm 1 (and only firm 1 ) had a marginal and average cost of $10. How would the equilibrium change? How does this compare to the Bertrand result when the firms sell perfect substitutes?

a. The price of the other good increases the firm's own demand.

b. pi = (pj +50)/2

c. p = 50 = Q

d. It would shift out that firm's BR function, but it would still be able to compete.

Demand curves are downward sloping—not horizontal. The firm with the higher marginal cost is not forced out of the market necessarily.

You might also like to view...

Use the following table to answer the question below. Jorge's Production Possibilities SchedulePounds of Green BeansPounds of Corn03202024040160608080 0 If Jorge produces 20 pounds of green beans, he can produce ________ pounds of corn.

A. 160 B. 240 C. 0 D. 80

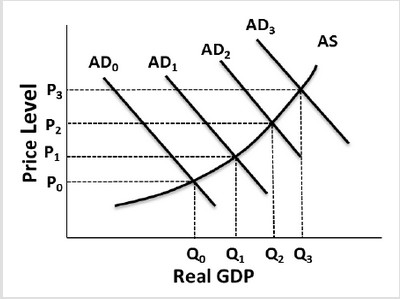

Use the following graph to answer the next question. Suppose the economy is currently in equilibrium at the full-employment real GDP level of Q2.and price level of P2. If an event occurred in the economy that triggered demand-pull inflation, we would expect

Suppose the economy is currently in equilibrium at the full-employment real GDP level of Q2.and price level of P2. If an event occurred in the economy that triggered demand-pull inflation, we would expect

A. the price level to move toward P3, and the output level to move toward Q3, B. the price level to move toward P3, and the output level to remain constant. C. the price level to move toward P1, and the output level to move toward Q1, D. the price level to move toward P1, and the output level to remain constant.

Explain the relationship between the aggregate supply curve and the Phillips curve

What will be an ideal response?

Planned investment is the:

A. amount that firms decide to allocate to inventory accumulation. B. spending households engage in based on forecasted budget. C. investment that a firm decides upon as a result of temporary market changes. D. amount that firms decide to allocate to new capital resources and inventory accumulation.