Scarcity is a situation in which resources are limited in quantity and can be used in different ways.

Indicate whether the statement is true or false.

Answer: False.

You might also like to view...

The costs associated with recalculating prices and printing new price lists when there is inflation are known as

A) menu costs. B) diminishing costs. C) shoe leather costs. D) chain-index costs.

In 2002, government expenditures as a percentage of GDP were lowest for which country?

a. Sweden b. United States c. Germany d. France

Corporate profits are

A. taxed twice-once by the corporate tax system, and again by personal tax system when they are paid to stockholders as dividends. B. taxed three times-once by the corporate tax system, again by the personal tax system, and again as capital gains. C. taxed only when a stockholder sells his or her shares of stock. D. taxed at too low a rate.

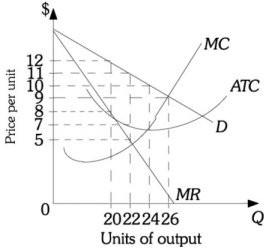

Refer to the information provided in Figure 13.4 below to answer the question(s) that follow.  Figure 13.4Refer to Figure 13.4. The profit-maximizing price for this firm is

Figure 13.4Refer to Figure 13.4. The profit-maximizing price for this firm is

A. $5. B. $7. C. $9. D. $11.